Nickel Metal Hydride Battery Industry Trends & Future Outlook (2026–2030)

Author: Weijiang Energy R&D & Market Research Team | Data Source: GEP, Straits Research, EU Regulation 2023/1542, MIIT 2025 Policies | Reading Time: 10 Mins

Against the dual backdrop of global carbon neutrality and diversified energy storage demand, the nickel metal hydride (NiMH) battery industry is entering a structural differentiation cycle. Unlike lithium-ion batteries focused on full electric vehicles, NiMH’s core competitive advantages lie in ultra-wide temperature adaptability, intrinsic safety, low carbon manufacturing and high recyclability. This paper sorts out verified global market data, iterative technology routes, two core regional policy frameworks (China new energy policy + EU circular economy rules), segmented growth tracks and investment logic for industry investors, policy researchers and OEM business decision-makers.

Traditional perception that NiMH is a shrinking consumer battery product has been overturned by emerging tracks including hybrid vehicles, industrial standby energy storage, polar & vehicle backup power. We analyze real industry data rather than vague predictions to clarify the 5-year development trajectory and hidden growth opportunities of the NiMH sector.

1 Global NiMH Market Scale & Segmented Growth Data (2025–2030)

Core Global Market Metrics

| Application Segment | 2025 Market Share | 2025–2030 CAGR | Core Growth Driver |

|---|---|---|---|

| HEV Hybrid Vehicles | 47.5% | 9.1% | Global hybrid vehicle penetration growth |

| Industrial & Energy Storage | 18.9% | 11.5% | Grid frequency regulation, base station backup |

| Special Extreme Equipment | 16.4% | 10.8% | Polar, desert, vehicle T-BOX power |

| Power Tools & Medical | 12.2% | 4.3% | Stable mature replacement demand |

| Consumer Small Devices | 5.0% | 2.8% | Slow growth, market shrinkage |

Key industry judgment: Consumer NiMH markets are gradually shrinking, while industrial, automotive and extreme-environment power supplies become high-growth core tracks. The industry is shifting from volume competition to high-value, customized wide-temperature NiMH solutions.

2 Core Technology Innovation Trends Of NiMH Batteries

R&D investment of global NiMH enterprises focuses on four major technical routes, with clear commercialization timelines supported by laboratory and mass-production data:

2.1 Wide Temperature Low Self-Discharge Cell (Mass Production Mature)

Composite anti-freeze electrolyte + modified AB5 hydrogen storage alloy solves electrolyte crystallization at -40℃. Mass-produced cells achieve stable discharge from -40℃ to 85℃, monthly self-discharge rate below 8%. This technology is the core competitive edge of Chinese OEM factories for T-BOX, polar exploration and desert solar storage packs, and is fully covered in Weijiang’s AAA/AA/SC mass production lineup.

2.2 High-Cycle Industrial Grade Alloy Materials

New rare earth bimetallic alloy achieves over 5,000 shallow charge-discharge cycles under HEV working conditions, far exceeding IEC 61951 standard requirements. Dry electrode coating technology cuts manufacturing energy consumption by 68% and eliminates wastewater discharge, matching global green factory certification standards.

2.3 Intelligent BMS Matching System Popularization

AI adaptive equalization algorithms control single cell voltage deviation within ±5mV, improving pack overall service life by 15%. BMS with NTC temperature sensor becomes standard configuration for vehicle and industrial wide-temperature NiMH packs.

2.4 Solid-State NiMH (Lab To Mid-Term Pilot)

Solid polymer electrolyte replaces liquid alkaline solution; lab energy density reaches 180Wh/kg. Industry consensus predicts small-batch trial production in 2028–2031, and will reshape high-end industrial battery competition patterns after mass production.

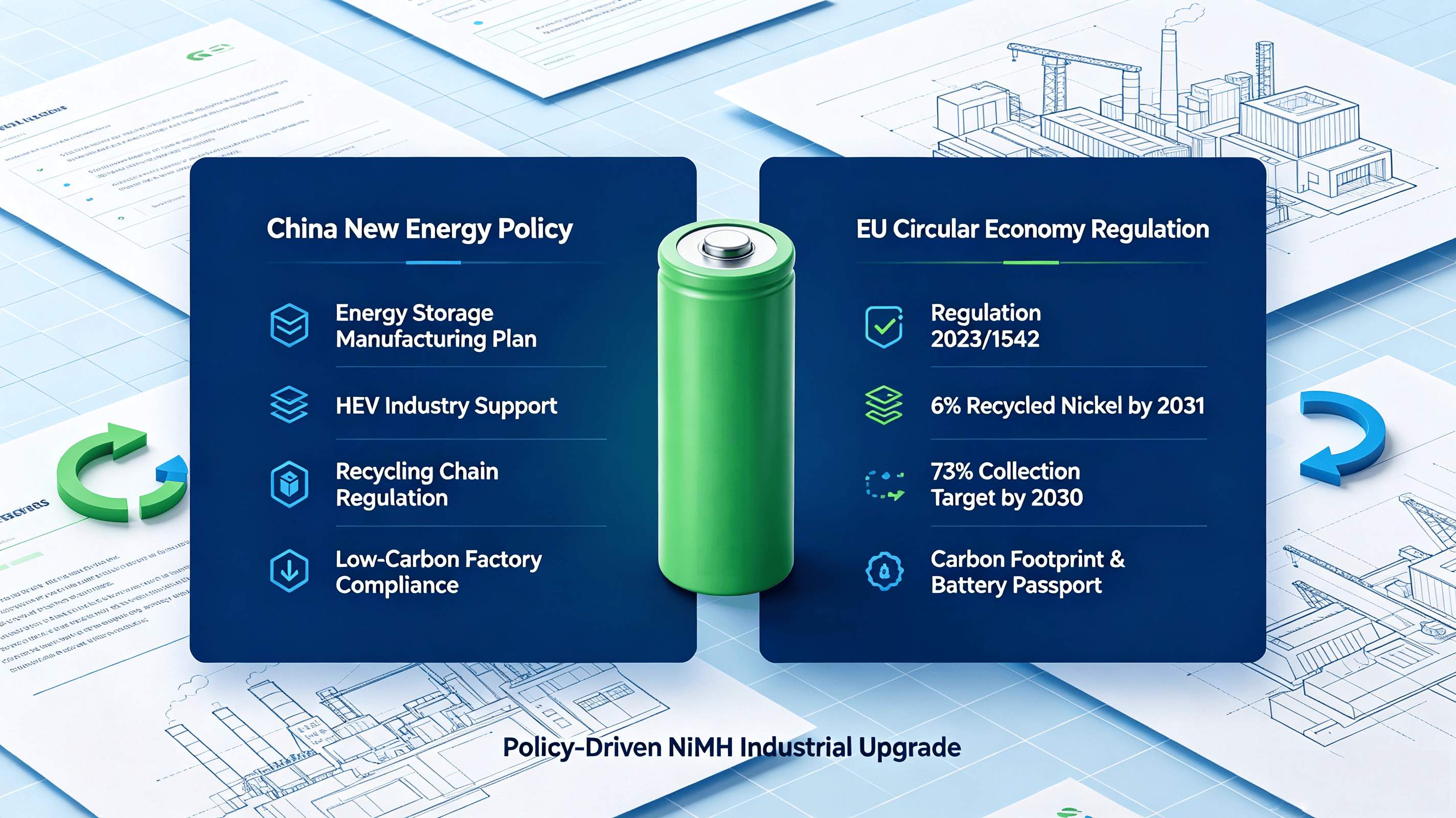

3 Policy Framework: China New Energy Policy Impact

Core Chinese Policy Documents (2025 Official Release)

- Action Plan For High-Quality Development Of New Energy Storage Manufacturing (2025–2030): NiMH is designated as key secure short & medium energy storage technology; support automated wide-temperature cell production lines with fiscal subsidies.

- New Energy Vehicle Industry Plan (2026–2035): HEV technical route receives sustained policy support, creating stable domestic NiMH vehicle demand.

- Revised NiMH Industry Specifications: Clear quantitative indicators for production carbon emission and battery recycling rate, pushing backward small factories to exit the market.

- Waste Battery Recycling Management Measures: Standardize nickel & rare earth regenerative recovery industrial chain, reduce raw material cost volatility for manufacturers.

Policy dividend analysis: Chinese domestic policy forms a complete closed loop of "production support + downstream demand + recycling system", accelerating the concentration of the NiMH industry. Top manufacturers with full R&D and customized pack capacity will expand market share continuously; small factories lacking wide-temperature technology and recycling matching will face elimination pressure after 2027.

4 EU Circular Economy Battery Regulation Requirements (Global Export Core Constraint)

EU Regulation (EU) 2023/1542, fully effective in 2027, sets binding lifecycle rules for all batteries imported into Europe, bringing both compliance costs and market barriers & opportunities for NiMH manufacturers:

- Mandatory recycled nickel content: 6% minimum by 2031, rising to 15% in 2036, creating stable demand for NiMH recycling raw materials;

- Portable battery collection target: 73% recovery rate by 2030, NiMH material recovery standard set at 80%;

- Full life carbon footprint declaration + battery passport required for industrial & automotive NiMH packs exported to EU;

- Restrict harmful substances: NiMH without cadmium, lead, mercury has natural compliance advantages vs lithium and nickel-cadmium batteries;